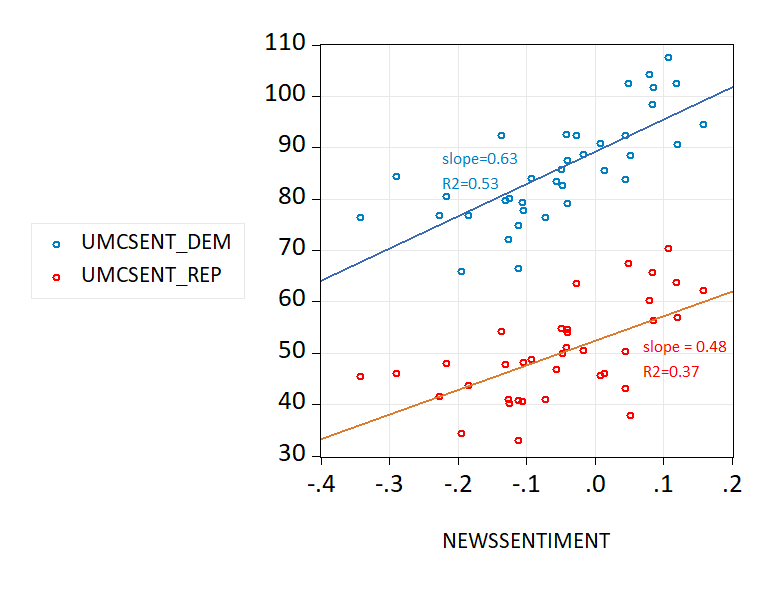

How sensitive are economic sentiments as measured by the University of Michigan survey, depending upon party affiliation? Apparently, over the period of the Biden administration, it’s higher for Democrat and lean-Democrat.

Figure 1: University of Michigan sentiment by Democrat/lean-Democrat (blue circles), by Republican/lean Republican (red circles) vs. Shapiro-Sudhof-Wilson SF Fed news sentiment index, 2021M02-2024M02. OLS regression lines (slope, R2) Source: University of Michigan, SF Fed, and author’s calculations.

Not only is Democrat/lean Democrat sensitivity greater, the R2 of regression of sentiment on news sentiment is higher too. In other words, it’s a little harder to link Republican/lean Republican sentiment to a text-based news index. The constant is statistically significant, whereas the slope coefficients are not significantly different, using the 5% significance level (F-test).

I also show a nonparametric smoother (nearest neighbor, window=0.7):

Figure 2: University of Michigan sentiment by Democrat/lean-Democrat (blue circles), by Republican/lean Republican (red circles) vs. Shapiro-Sudhof-Wilson SF Fed news sentiment index, 2017M02-2024M02. Nearest neighbor fit lines (window =0.7) Source: University of Michigan, SF Fed, and author’s calculations.

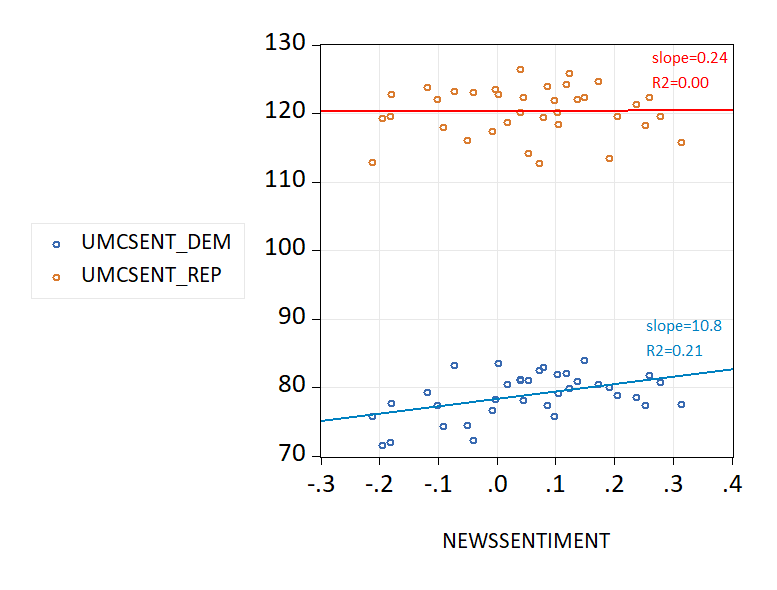

Note that this relationship held even more strongly during the Trump administration, pre-pandemic:

Figure 3: University of Michigan sentiment by Democrat/lean-Democrat (blue circles), by Republican/lean Republican (red circles) vs. Shapiro-Sudhof-Wilson SF Fed news sentiment index, 2017M02-2020M01. OLS regression lines (slope, R2) Source: University of Michigan, SF Fed, and author’s calculations.

During the Trump administration, Republican/lean-Republican economic sentiment as measured by the Michigan survey was essentially completely unexplained by news sentiment as measured by the Shaprio-Sudhof-Wilson index. (The slope coefficient for Democrat/lean-Democrat is statistically significantly different from zero using HAC robust standard errors.)

Source link