From Zerohedge

Given the long lag between recessionary indicators and economic recession, it is unsurprising economists gave up anticipating a recession. However, while the recession has not happened yet, it does not mean that it still can’t. We should pay special attention to data historically correlated to economic growth.

To recap, here are the indicators that the NBER uses to determine peaks and troughs, although not in “real time”.

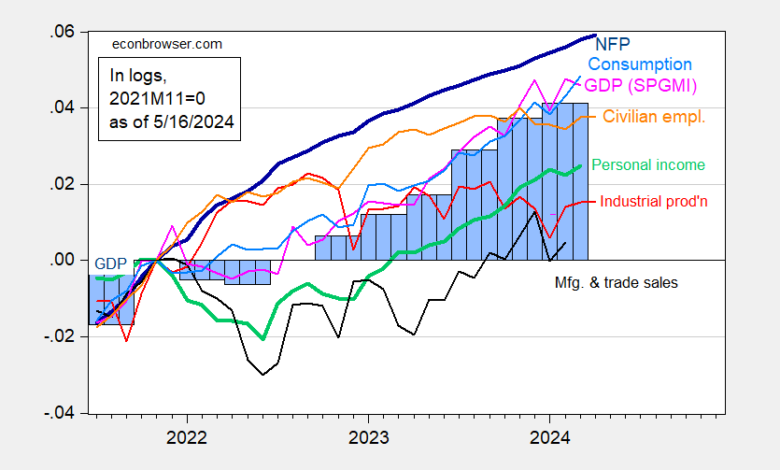

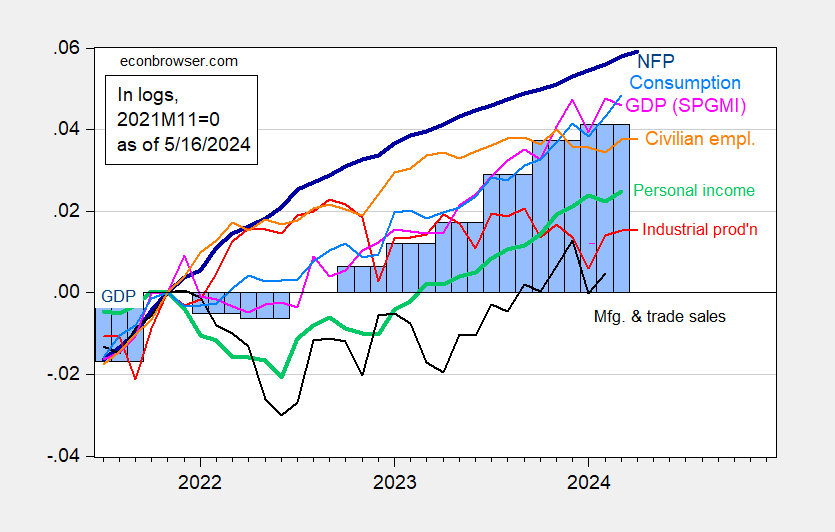

Figure 1: Nonfarm Payroll (NFP) employment from CES (bold blue), civilian employment (orange), industrial production (red), personal income excluding current transfers in Ch.2017$ (bold green), manufacturing and trade sales in Ch.2017$ (black), consumption in Ch.2017$ (light blue), and monthly GDP in Ch.2017$ (pink), GDP, 3rd release (blue bars), all log normalized to 2021M11=0. Source: BLS via FRED, Federal Reserve, BEA 2024Q1 advance release, S&P Global Market Insights (nee Macroeconomic Advisers, IHS Markit) (5/1/2024 release), and author’s calculations.

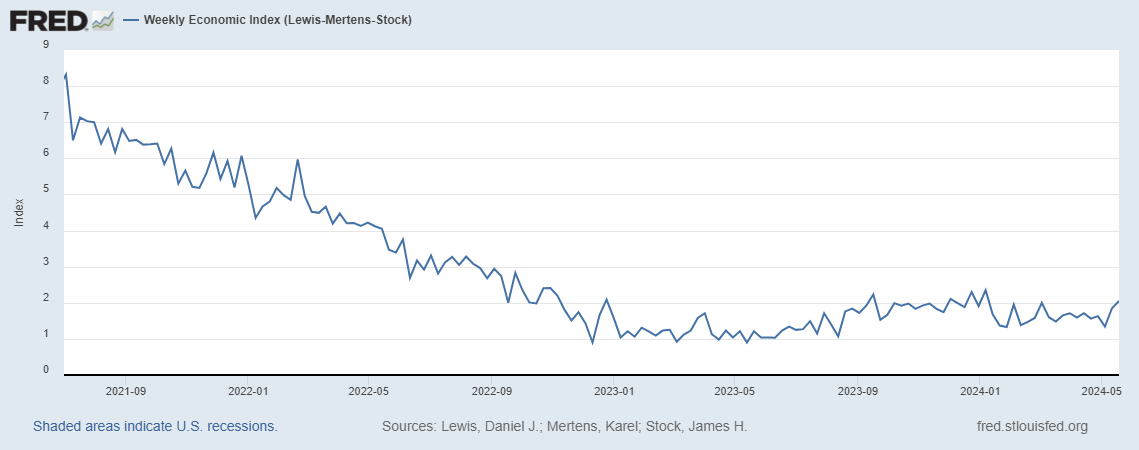

Everybody has their favorite indicator – Vehicle Miles Traveled, gasoline consumption, growth of full time workers, and so forth. I’ll just observe that the Lewis-Mertens-Stock Weekly Economic Index shows 2.05% — just at trend if trend is 2% — using data released through 18th of May.

The Baumeister, Leiva-Leon, Sims Weekly Economic Conditions Indicator registers -0.52% (i.e. about half a point below trend growth).

So the recession could still appear, maybe six months from now, maybe next month. A simple plain vanilla term spread model says May is the highest likelihood for a recession so it still could happen. Or not.

Source link