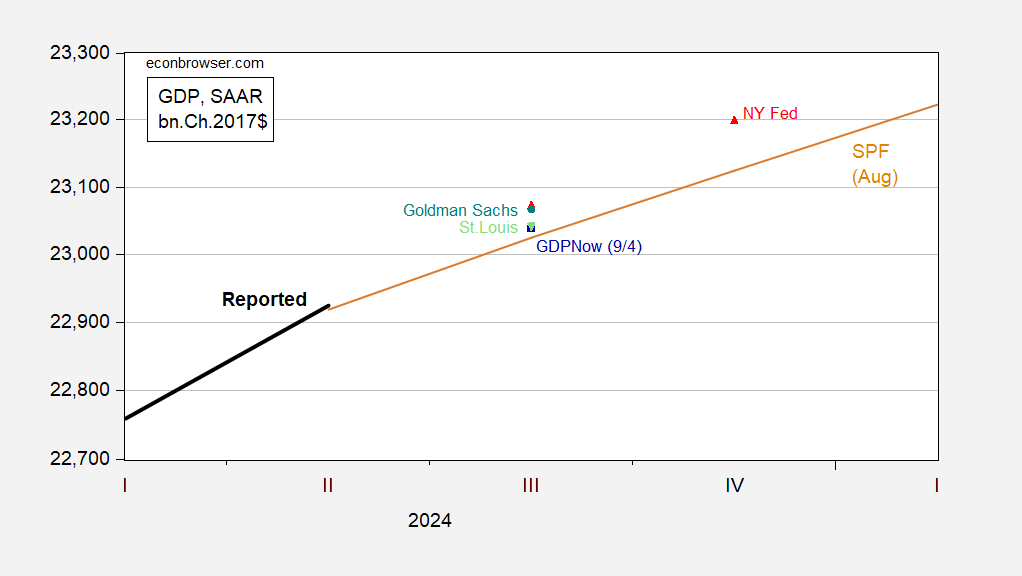

We have plenty of competing assessments as of today. From three Federal Reserve Banks and Goldman Sachs.

Figure 1: GDP (bold black), Survey of Professional Forecasters August median forecast (tan), GDPNow (blue square), NY Fed (red triangle), St. Louis Fed (light green inverted triangle), Goldman Sachs (teal circle), all in bn.Ch.2017$. Nowcasts are as of 9/6 except where noted; nowcast levels calculated iterating growth rate to reported 2017Q2 2nd release GDP levels. Source: BEA 2024Q2 2nd release, Philadelphia Fed for SPF, Atlanta Fed (9/4), NY Fed (9/6), St. Louis Fed (9/6), Goldman Sachs (9/6), and author’s calculations.

In addition, S&P Global Monthly Insights (formerly Macroeconomic Advisers) reports 2.0% growth as of 9/3, slightly below the 2.1% from GDPNow

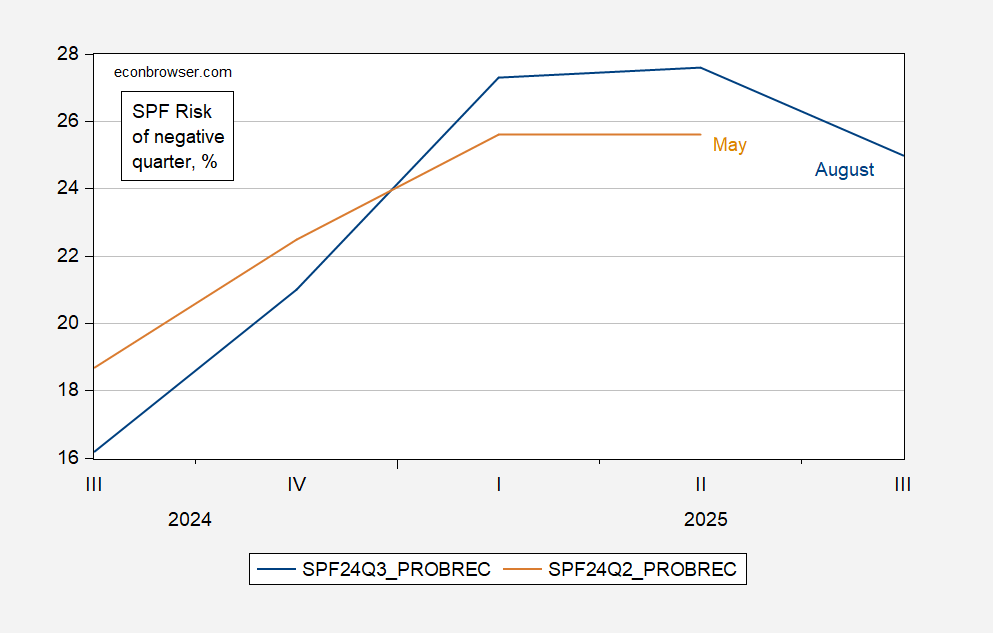

The upwards revision in Q2 GDP plus subsequent information has pushed nowcasts uniformly above the SPF median forecast (reported by early August). It’s hard to see how short horizon assessments of recession likelihoods have increased. For comparison, here are the early August forecasts likelihoods from SPF:

Figure 2: Risk of negative quarter growth, from August survey (blue), from May survey (tan), both in %. Source: Philadelphia Fed.

Recession probabilities down in near quarters (Q3, Q4), up in far (2025Q1, Q2).

Source link