I’m taking the WSJ’s word for it, from the article “Russia’s War Economy Shows New Cracks After the Ruble Plunges”.

The Russian economy, surprisingly resilient through two-plus years of war and sanctions, has suddenly begun to show serious strains.

The ruble is plunging. Inflation is soaring, and President Vladimir Putin told the Russian people this week that there isn’t any reason to panic.

The catalyst for the change in economic fortunes was a decision by the Biden administration to ratchet up sanctions on Russia’s Gazprombank, the last major unsanctioned bank that Moscow uses to pay soldiers and process trade transactions, as well as more than 50 other financial institutions.

While official statistics have certainly depicted a surprisingly resilient Russian economy, there are definitely questions regarding it’s true strength (remembering that “Potemkin village” is a term originating from that country). First the plunge in the ruble indicates the tradeoff that is being made between defending the currency, staunching inflation and keeping the economy growing.

Bofit, a week ago, highlighted the deceleration in y/y growth:

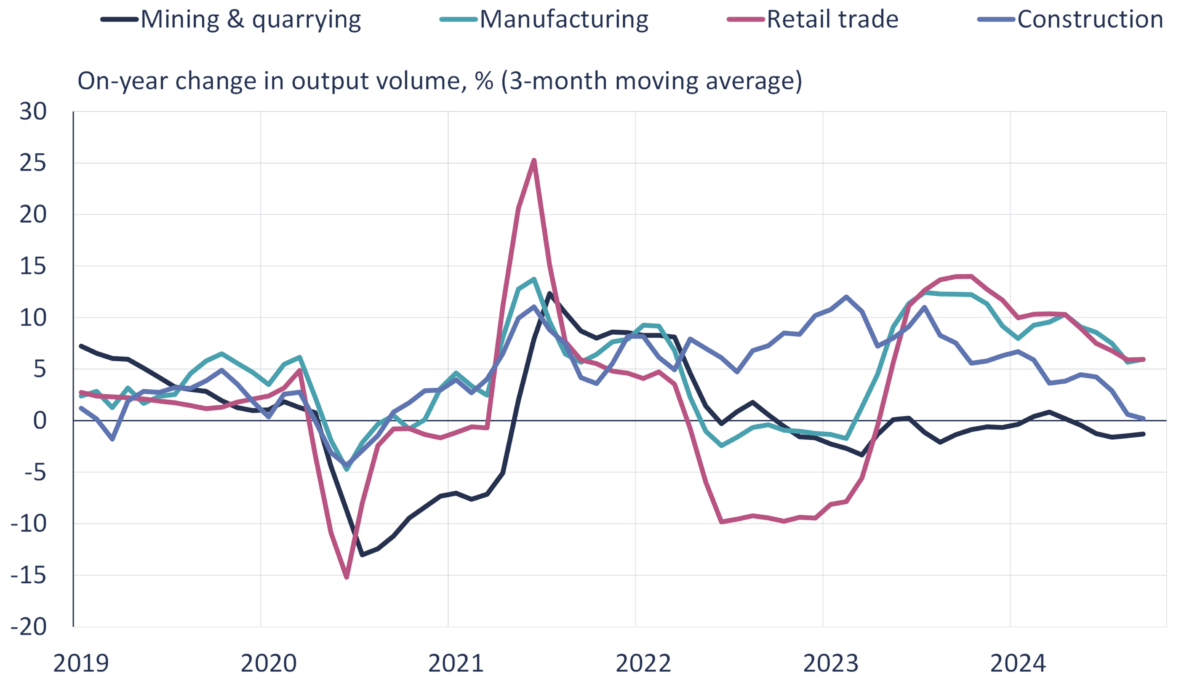

Russian GDP growth slowed significantly in the third quarter

Rosstat’s preliminary estimate puts Russian GDP growth in July-September at 3.1 % y-o-y. GDP growth has slowed significantly this autumn. All core sectors have shown weaker growth in recent months compared to the first half of this year.

The slowdown in GDP growth has largely been driven by pressures from the mining & quarrying and construction sectors. On-year output of mineral extraction industries (includes oil & gas) has fallen in recent months, while on-year growth in construction is practically zero. Agricultural output also contracted in the third quarter. GDP growth has still been supported by manufacturing and retail sales, but growth has slowed also in these branches. Manufacturing growth, in turn, has been driven mainly by industries related to war.

Here’s their graph, using official statistics:

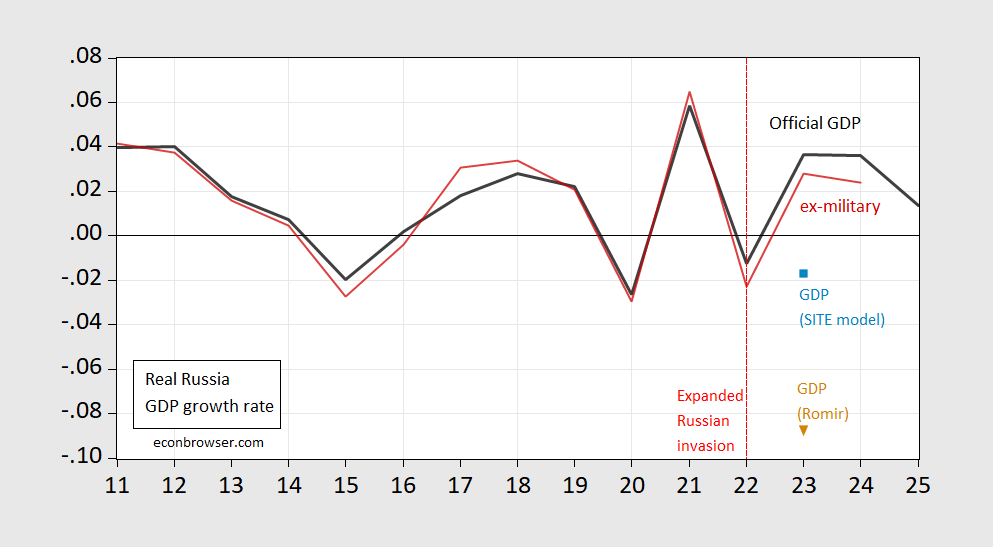

Finally, let’s think about the plausibility of Russian statistics, and also what GDP measures. First, compare official GDP to official GDP ex-military spending (as estimated by SIPRI):

Figure 1: Official Russian GDP growth (black), official GDP ex-military spending growth (red), Russian GDP using SITE oil-based model (light blue square), official GDP using Romir price index as deflator (tan inverted triangle). GDP ex-military spending calculated using nominal values, deflating by overall GDP deflator. Source: IMF October 2024 WEO, SIPRI database, SIPRI, SITE (Figure 26), and author’s calculations.

The strong growth looks less strong when deducting outright military expenditures (note that capital costs associated with defense spending, along with other internal security operations, would not be included in SIPRI’s estimates of military expenditures).

In addition, the Stockholm Institute of Transition Economies, in it’s recent report on the Russian economy, provides several alternative estimates of Russian GDP growth. I show two estimates: (i) one based on a simple econometric model linking oil prices to Russian GDP, and (ii) nominal GDP deflated by the Romir price index (see this post).

Source link