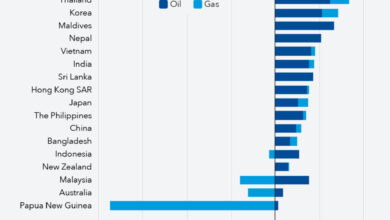

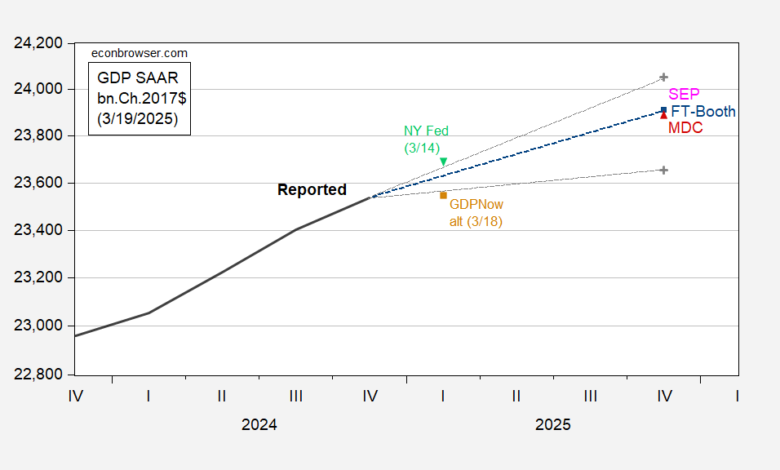

The March FT-Booth survey is out; median q4/q4 growth for 2025 is 1.6%, down from 2.3% in the December survey (see this post for comparison to FOMC SEP, the median entry is 1.7%). The average 90th/10th bounds are also interesting, in that large downside risks are perceived.

Figure 1: GDP as reported (bold black), March FT-Booth median (blue square), 90/10 percentile bounds (gray dashed lines, gray +), Chinn forecast (red triangle), GDPNow of 3/18 adjusted for gold imports (brown square), NY Fed nowcast of 3/14 (inverted green triangle) all bn.Ch.2017$ SAAR. Source: BEA, FT-Booth, Atlanta Fed, NY Fed, and author’s calculations.

The average 10th percentile reading is 0.5% q4/q4 growth, down from 2.0% in December (!).

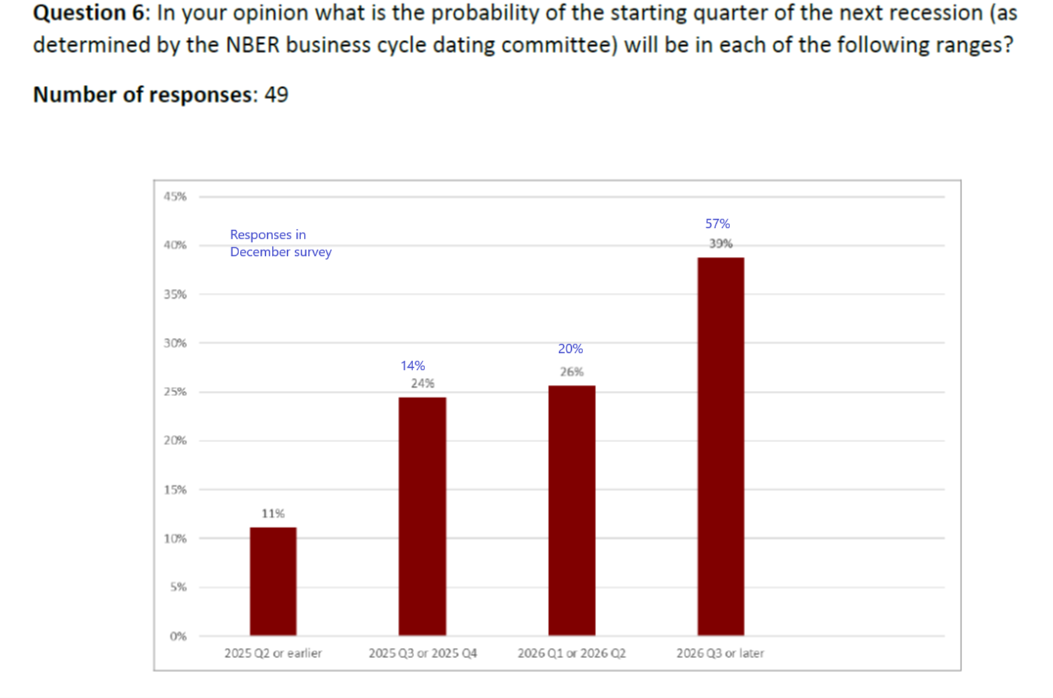

Respondents’ modal response for recession start is still 2026Q3, but ascribe a higher likelihood to an earlier start.

Notes: Proportion of responses in March survey. Percentages in blue indicate December survey.

The proportion of respondents who believe a recession begins in the second half of 2025 have risen from 14% to 24%, in the first half of 2026 from 20% to 26%. That means half of the respondents believe a recession will have started by 2026H1, up from 36%.

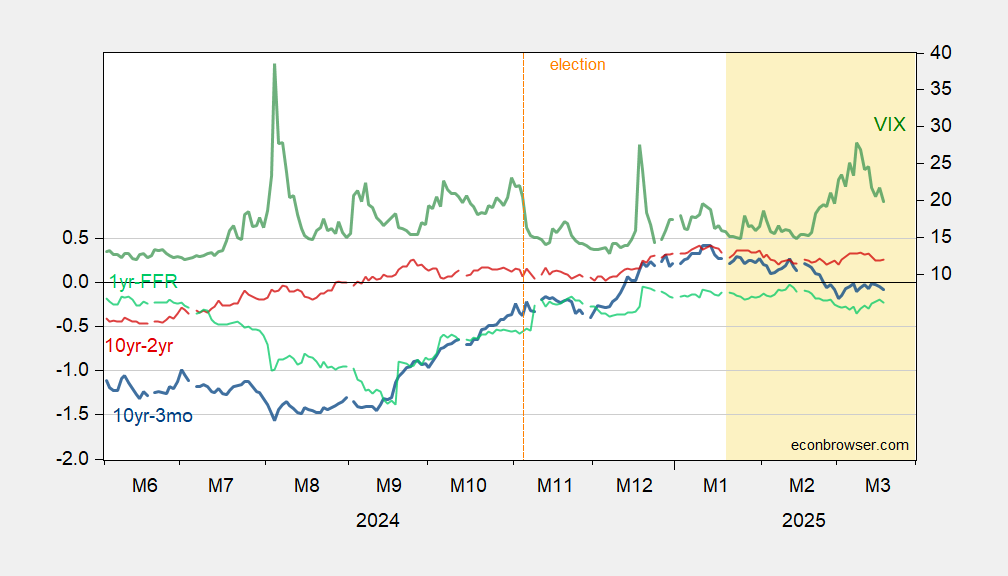

As of yesterday’s close, the 10yr-3mo Treasury spread is -8 bps, having inverted since inauguration day.

Figure 2: 10yr-3mo Treasury term spread (blue, left scale), 10yr-2yr Treasury term spread (red, left scale), 1yr-Fed funds spread (light green, left scale), all in %, VIX at close (green, right scale). Source: Treasury, CBOE via Treasury.

Source link