Kevin Hassett noted on Face the Nation yesterday:

HASSETT: …look at [oil] futures markets, which are interesting because you’ve cited over and over the spot price of gasoline, which, of course, is affected right now by the disruption of the strait, but if you look at the futures prices, they are expecting a rapid, rapid end to the situation and much, much lower prices. In fact, I don’t think I’ve seen a sort of future price path with such a steep decline in all my years watching futures.

It’s true that the futures are about as good as one gets in terms of predicting future oil prices; see Chinn and Coibion (2014), discussion in this post. I recall while serving in the government, futures were used as a quick and dirty guide to expectations regarding oil and other commodity prices.

And Hassett is correct that futures indicate a decline (rapid? That’s a matter of judgement).

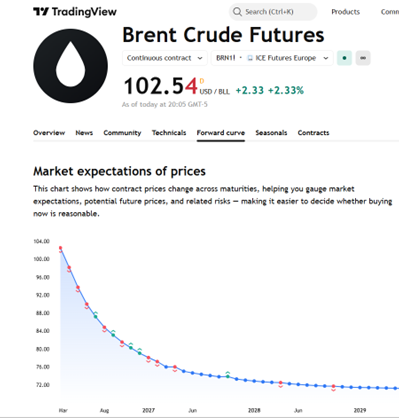

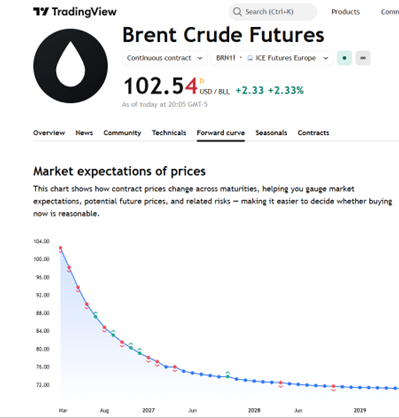

I’ll note that the forward curve does not return to the prewar price of $73 until sometime in 2027…

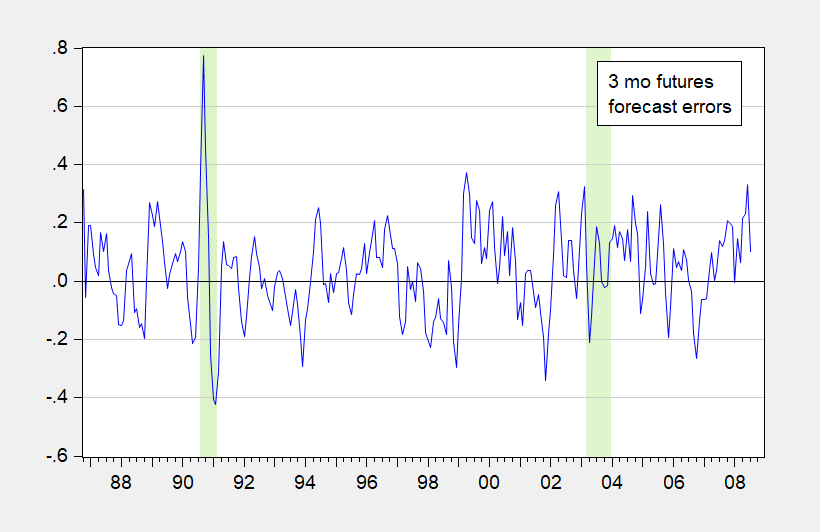

While futures incorporate market expectations, they are essentially of little predictive power during wartime (Gulf War I, Gulf War II thru capture of Saddam Hussein).

Figure 1: Front month oil futures to 3 month futures lagged 3 months, log ratio (blue). War periods shaded light green. Source: NYMEX via Chinn and Coibion (2014).

A regression of price on 3 month lagged futures during has an adjusted R2 of 0.94 during non-war periods, and 0.12 during war periods. While not surprising, it’s useful to remember that futures in this context need not be very predictive.

Source link