The forecast will be the same as reported in the Budget (see here), using data from November. Hence, will be OBE given slowdown pre-War, and post-War cost-push shock.

However, I expect a more fulsome explanation for why the Administration forecast deviated from roughly contemporaneously finalized forecasts, as shown below.

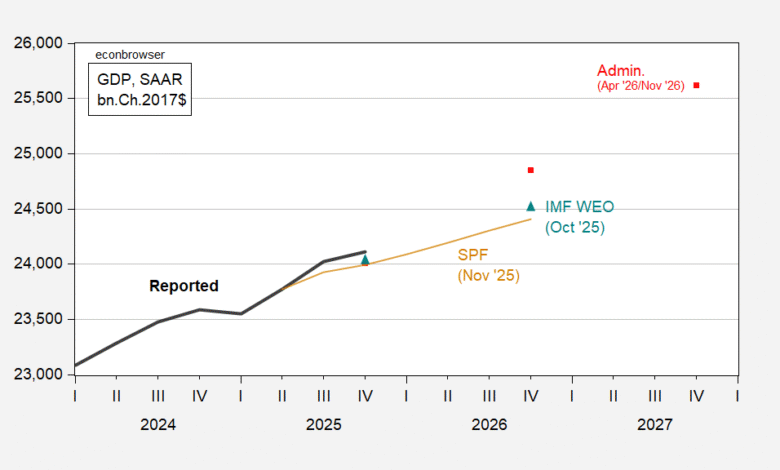

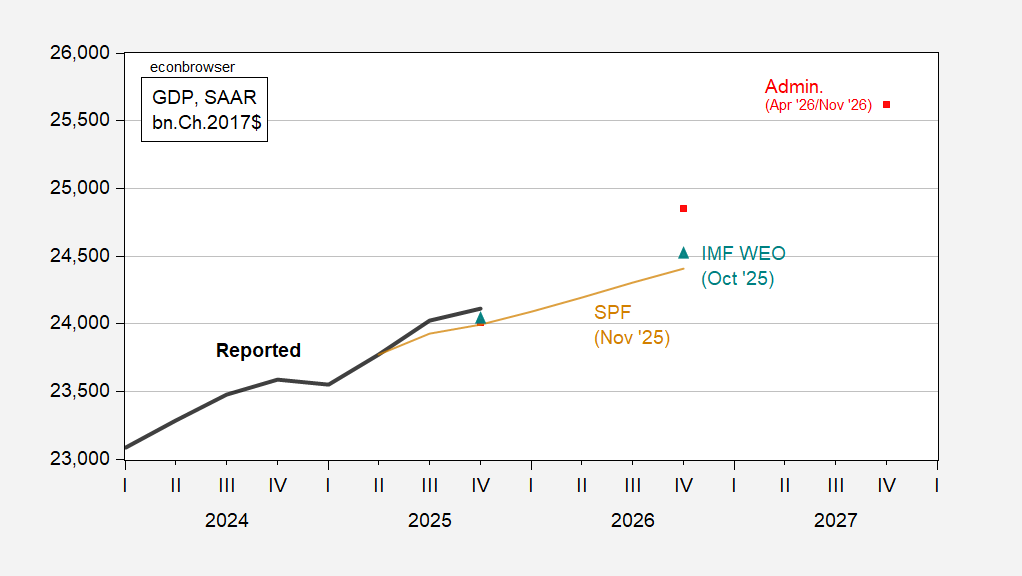

Figure 1: GDP (bold black), April Admin. 2026/Nov. 2025 (red square), November 2025 Survey of Professional Forecasters (brown), IMF October WEO (teal triangle), all in bn.Ch.2017$ SAAR. Source: BEA, OMB, IMF WEO October update, Philadelphia Fed, and author’s calculations.

As for topics, my guess — see recent reports (purely a guess — I have no contacts in the current CEA).

Source link