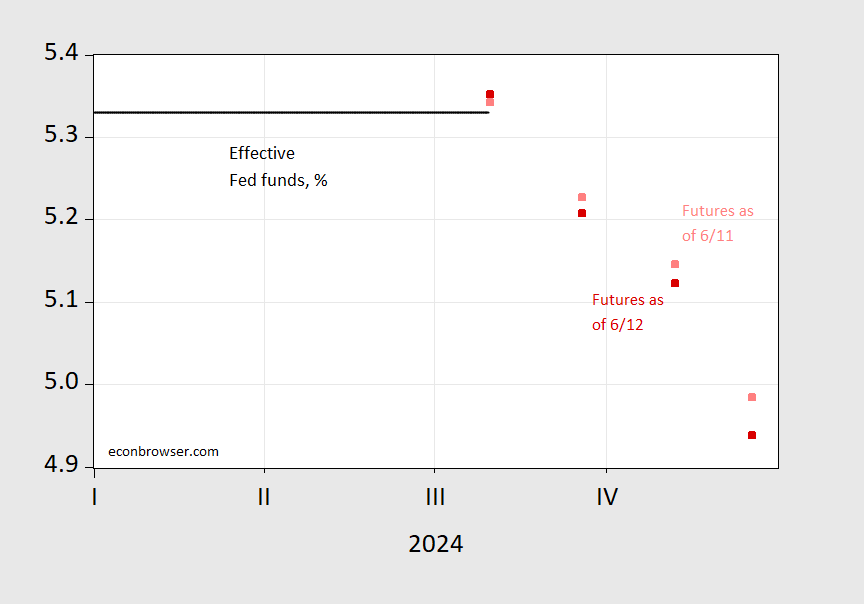

Here’s a picture of the Fed funds pre- and post-CPI release/FOMC SEP:

Source: CME accessed 6/12/2024, 1:30pm.

Before the news, the implied drop over 2024 was 35 bps, now 39 bps. How many drops? Using modal probabilities:

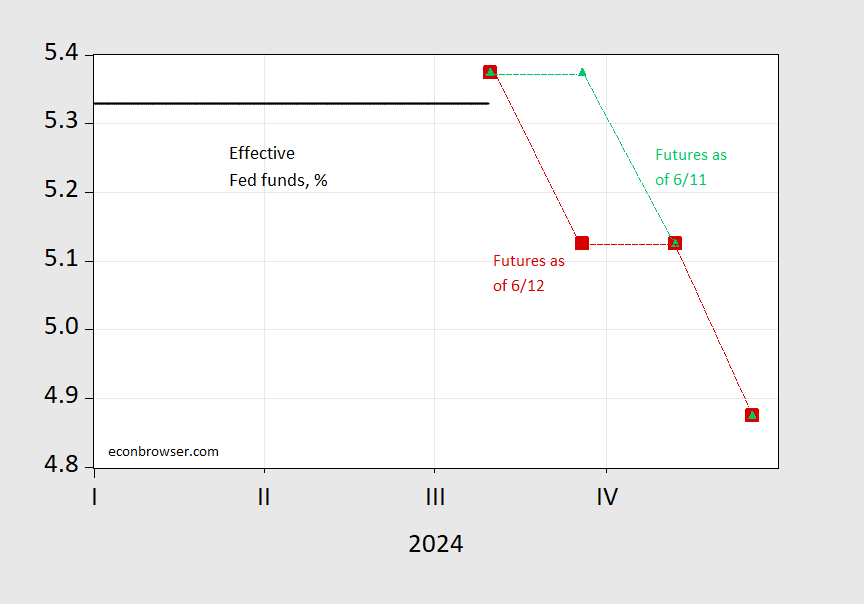

Source: CME accessed 6/12/2024, 1:30pm.

Two 25 bps drops before, two drops after the news.

Current commentary stresses that the close balance between one and two cuts in the SEP (see SEP here).

Market expectations (i.e., ex ante measures) are important for behavior. Which one will turn out to be more accurate in terms of forecasting. This issue is taken up in Carpinelli et al. (2024).

Source link