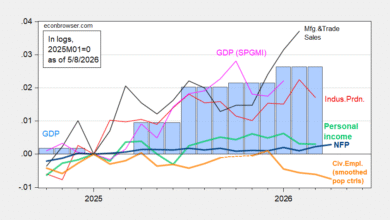

Despite the upward revision to Q2 GDP, and accelerated nowcast growth in 3rd quarter GDP, aggregate demand is decelerating.

First, GDP, the measurement of which we know has been distorted by tariff frontrunning:

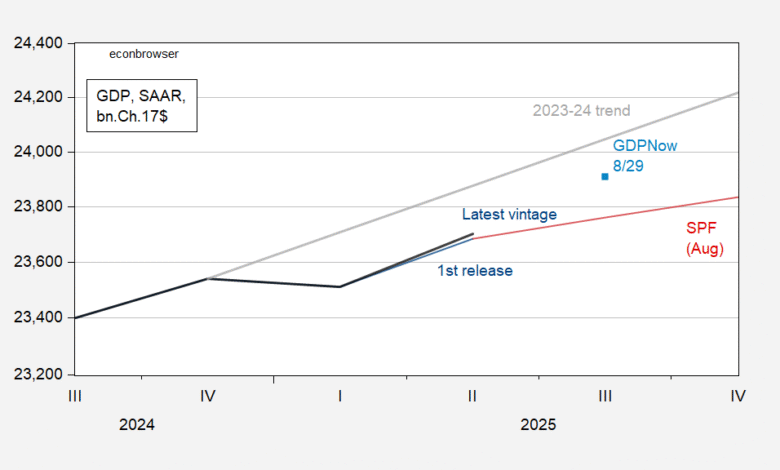

Figure 1: GDP, latest vintage (bold black), advance release (blue), GDPNow of 8/29 (light blue square), Survey of Professional Forecasters August median (dark red), 2023-24 stochastic trend (gray), all in bn.Ch.2017$ SAAR. Source: BEA, Atlanta Fed, Philadelphia Fed, and author’s calculations.

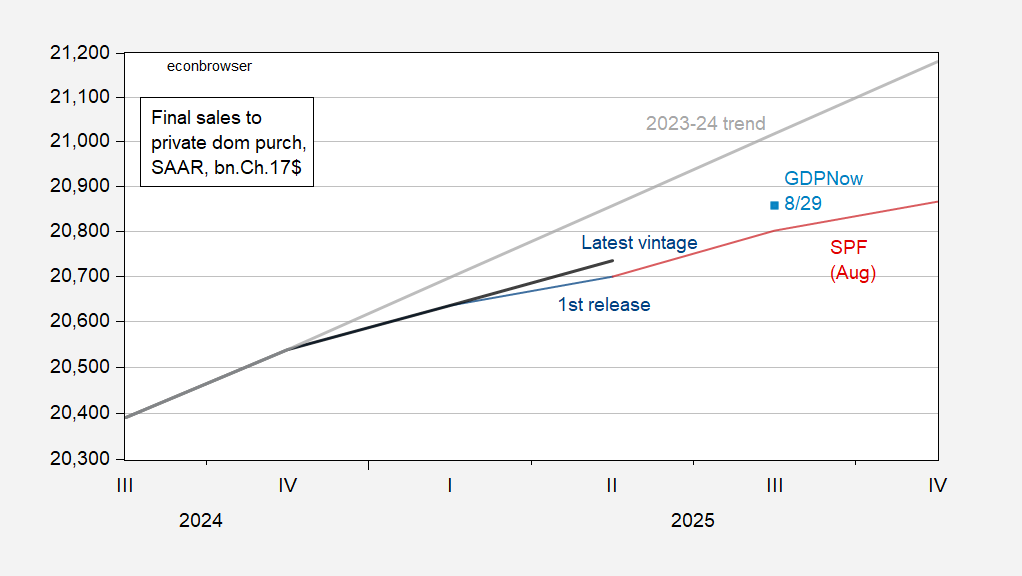

Q2 GDP growth (q/q AR) was revised up, and Q3 GDPNow was upped from 2.2%to 3.5%. Final sales to private domestic purchasers was increased, as was the Q3 nowcast.

Figure 2: Final sales to private domestic purchasers, latest vintage (bold black), advance release (blue), GDPNow of 8/29 (light blue square), Survey of Professional Forecasters August median (dark red), 2023-24 stochastic trend (gray), all in bn.Ch.2017$ SAAR. Source: BEA, Atlanta Fed, Philadelphia Fed, and author’s calculations.

Hence, there’s no big recovery in what Furman calls “core GDP” (essentially private domestic aggregate demand), in that we are not by any means returning to the 2023-24 trajectory.

Source link