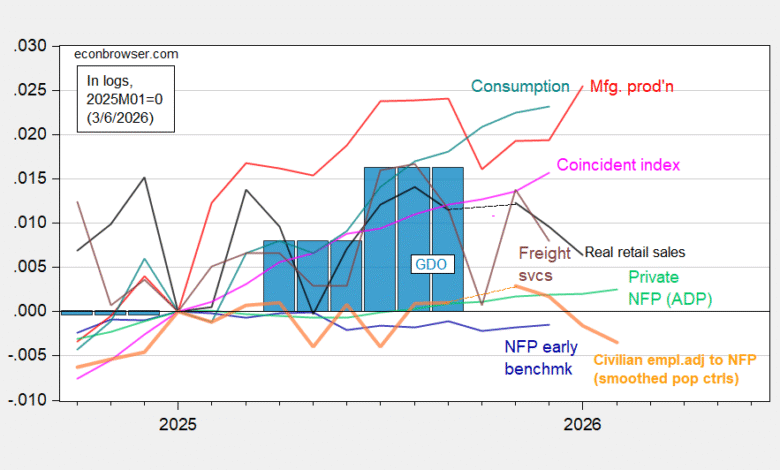

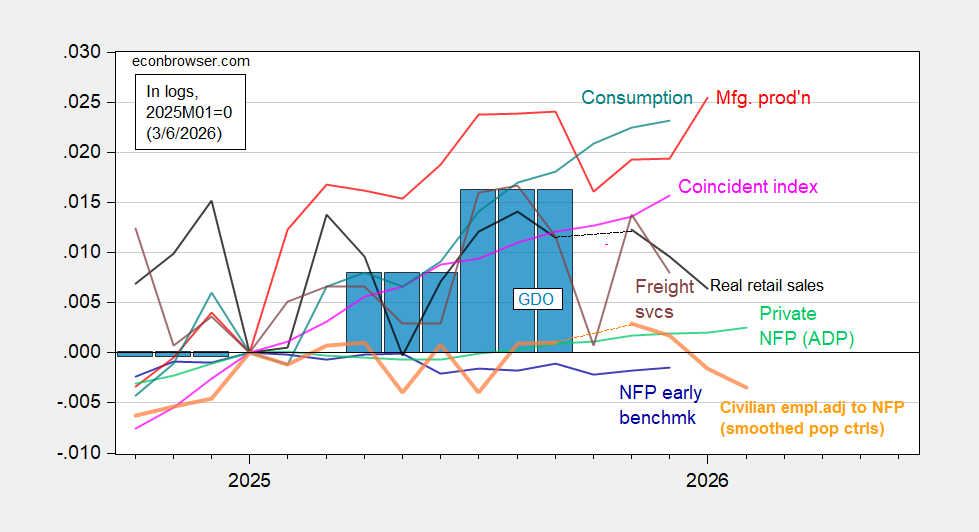

Civilian employment adjusted to NFP concept is diving (after retroactive application of 2026 population controls to January 2026 data), as are real retail sales in January.

Figure 1: Implied Nonfarm Payroll early benchmark (NFP) (blue), civilian employment adjusted to NFP concept, using smoothed population controls (bold orange), manufacturing production (red), private NFP from ADP (light green), real retail sales (black), freight services index (brown), coincident index in Ch.2017$ (pink), and GDO (blue bars), all log normalized to 2021M11=0. Retail sales deflated by CPI. Source: Philadelphia Fed [1], Philadelphia Fed [2], Federal Reserve via FRED, BEA 2025Q4 advance release, and author’s calculations.

The pattern of output measures diverging from employment — also displayed in the set of indicators focused on by the NBER’s Business Cycle Dating Committee (BCDC) — is replicated here. Notable observations: (1) Civilian employment adjusted to NFP concept is now on a pretty clear downswing, now that the 2026 population controls are applied to January’s data; (2) inflation adjusted retail sales are down as well.

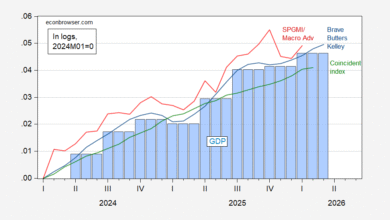

Nowcasts have been downshifted as well; GDPNow for Q1 dropped from 3.2% q/q AR yesterday to 2.1% today. NY Fed’s nowcast dropped from 2.4% last Friday to 2.2% today. Goldman Sachs tracking as of today stayed at 3.4%.

Source link