Friday’s jump in 10 year Treasury yields (10 bps), and the 30 year yield nearing 5% alarmed markets. But why?

Debt and the debt trajectory are up. Fed Chair Designate Warsh wants to shrink the Fed balance sheet, even as Trump continues his assault on Fed independence. And don’t expect the foreign sector to rush in to help…

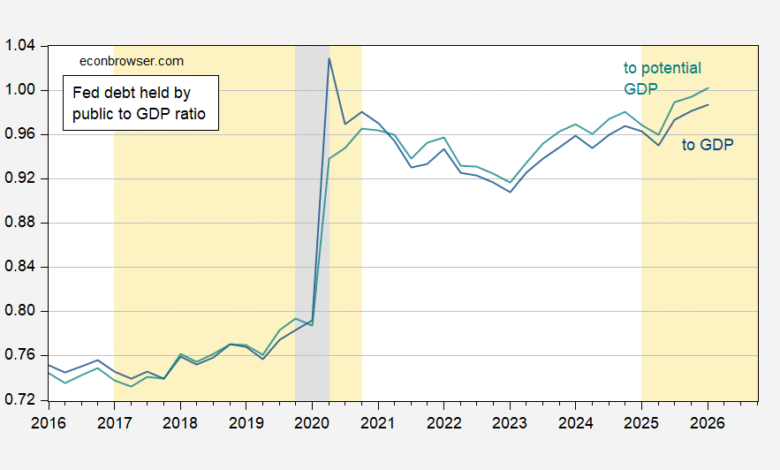

First, debt held by the public as a share of GDP:

Figure 1: Federal debt held by the public to GDP (blue), to potential GDP (teal). NBER defined peak-to-trough recession dates shaded gray. Source: Treasury, BEA via FRED; CBO (February 2026), NBER and author’s calculations.

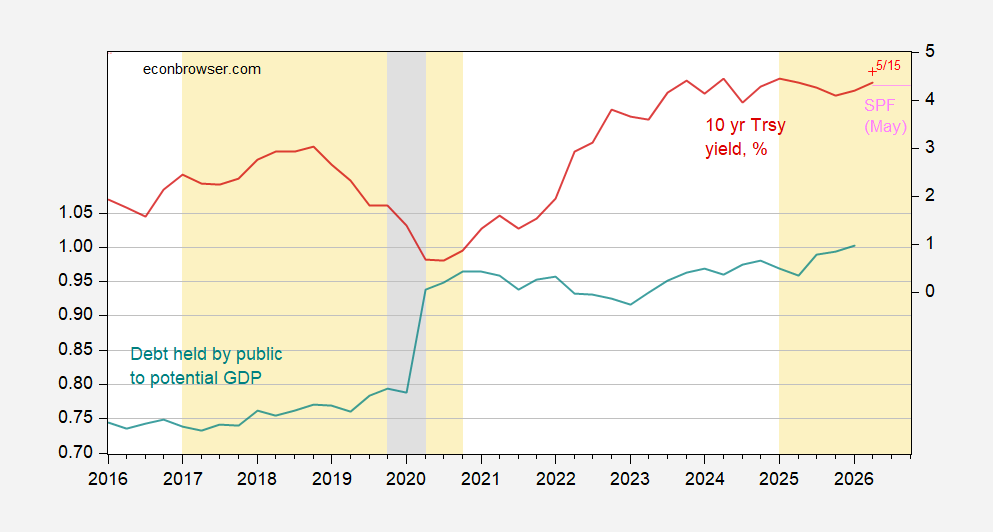

Second, debt and rates.

My work with Jeffrey Frankel (2005) indicates the debt to GDP ratio, expected changes in debt-to-GDP, expected inflation and output gap affect Treasury yields. This correlation is shown below.

Figure 2: Federal debt held by the public to potential GDP (teal, left scale), and 10 year Treasury yield (red, right scale), 5/15 COB observation (red +, right scale), SPF May mean forecast (pink, right scale), all in %. Q2 observation for 10 year yield is for data through May 15th. NBER defined peak-to-trough recession dates shaded gray. Source: Treasury, BEA via FRED; CBO (February 2026), Philadelphia Fed (May 2026), NBER, and author’s calculations.

Note that the 5/15 10 year yield has already jumped above the SPF forecast for Q2.

Subsequent work (Kitchen and Chinn, 2011) indicates that foreign holdings of Treasurys and Fed credit easing also play sigificant roles for rates. With newly confirmed Chair Warsh’s antipathy toward credit easing well-known, perhaps the timing of the rate rise might not be so surprising.

Source link